Over recent weeks inflation has been discussed extensively in the media. As usual they present the available information as a doomsday scenario, making projections for dire times ahead.

But the attention they’re giving inflation does mean it’s now on people’s radar. This is important because understanding the effect of inflation is critical to your financial planning success. This article explains the impact of inflation and the best way to stay ahead of it over the long term.

Most people perceive investments and market returns as the main risk they encounter when making long-term financial plans. But the real risk to your future lifestyle is inflation.

Inflation eroding our wealth – the challenge we face

We all have a sense that prices are going up, as indicated by inflation, although looking at a single item and how the cost of it has changed over time, can be helpful.

It’s hard to believe that a first-class stamp cost just 24p in 1992. Today, buying that same stamp costs you 85p.

This means that if you had kept your money in a bank account that pays virtually no interest, or under the proverbial mattress, your money would buy you a little over a third of the number of stamps today as it would have in 1991.

30 years seems a long time, but broadly speaking, this is the average life expectancy of someone who’s retiring today, so it’s a relevant timeframe to consider.

Taking this further, goods and services that cost you £1,000 in 1990 would have cost you £2,324 in 2020, according to the Bank of England inflation calculator, based on average inflation of 2.9% over the last 30 years. This means that over three decades, the value of your money has reduced in real terms by well over half, diminishing the purchasing power of your wealth.

So even if your lifestyle doesn’t change over your three-decade retirement, the cost of maintaining it will inevitably increase over time.

The silver lining of this is that in today’s value of money, it’s also reducing the value of your mortgage. This is because inflation means your salary is almost certain to increase in the future, but debts such as your mortgage won’t. So, inflation is effectively helping to reduce the present-day value of your long-term debts.

Cash should not be seen as an investment

Having some cash readily available to cover the unexpected cost of emergencies and income needs along with known expenditure for projects or goals for the next two to three years is important. But some people are inclined to keep far more than this in cash.

The wiring in our human brains means we are naturally averse to loss. Because we react much more strongly to a loss than we do to a gain, cash can seem a tempting sanctuary, but will cost you large sums of money in the long term.

According to website Money Saving Expert, the best interest rate available on a savings account at the time of writing this piece was 2.1% for a five-year fixed rate. This means committing to tying your money up for five years with the almost certain outcome that your money will not retain its purchasing power over that five year period.

Is that what you would consider safe, or a “dead cert” for a decline in value?

The answer – a smart strategy for long-term investing

Investing your money is fundamental to building and preserving your long-term wealth. Unfortunately, doing so requires navigating a minefield of jargon, apparent opportunities that really are too good to be true, and promises of future returns which are in fact unknown.

The best way to alleviate any inflation concerns you may have is to own a portfolio of globally diversified companies. You’ll be familiar with many of these companies as they are household names that we use in our daily lives.

The most successful companies thrive due to their constant innovation, in the quest for success and profit, and in doing so they drive positive long-term market returns.

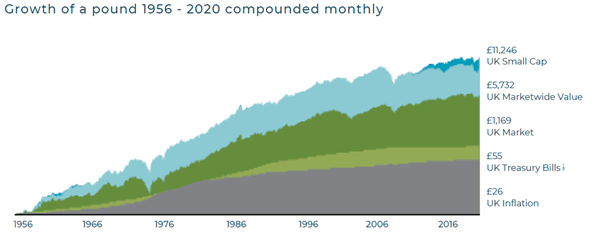

The chart below shows you how much a pound invested in 1956 would be worth in 2020 had it grown at the rate of inflation. You can see how this would have performed versus UK market returns.

Over the last 30 years, a client with a moderate appetite for investment risk who put their money in a smart investment strategy could have achieved returns of over 8% a year1. After all charges have been deducted, this leaves the investor well ahead of inflation which, as noted above, has averaged under 3% over that time period.

Investing in a highly diversified global portfolio reduces some aspects of investment risk, such as whether or not a specific stock or market is going to perform the way you hoped. But it will still be necessary to accept the short-term ups and downs that are an entirely normal part of market behaviour.

We like to compare it to watching someone going up an escalator playing with a yoyo. It’s important to focus on the escalator rather than the yoyo.

The Bank of England view on inflation is that it will continue to increase during the early part of this year, remaining high for 2022, then start to fall back towards their target of 2%. Of course, how accurate their projection for future rates is remains to be seen, so the best thing you can do is ensure you are best placed for whatever comes next.

If you would like to understand more about how smart investing can counteract the effects of inflation, contact us at your@lifemattersfp.flywheelstaging.com or call 01202 025481.

Please note, the value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Sources:

1 Based on the performance of the Life Matters EBI Portfolio – 60% Equity.